I have wanted to write this post for a while now. My partner and I recently moved out of our parents’ houses and we’re renting. Many people who know me voiced their shock at my decision to rent instead of buy a house. There were likely a number of reasons why they were shocked, and I imagine the main ones were:

- I originally planned on purchasing an investment property while I lived with my parents. I was going to renovate it, wait for it to appreciate in value, then either use the equity as a deposit on another house to live in, or live in the first house and stop renting it out as an investment. People who were aware of this plan noticed the change.

- I am known to be “good with money”. In these people’s eyes, I have made a silly decision to burn money renting instead of putting the money into owning a home.

- People who don’t know me well probably just make the assumption that I couldn’t afford to buy, so I settled for renting.

This post will go into the pros and cons of renting vs buying a house, as well as the specific reasons why I’m renting.

Owning a House Is Overrated

Property is a big thing in Australia. It’s one of the reasons we have such high house prices. There seems to be a general expectation that you go to school, go to university, get a good job, save for a deposit, and move out into your own house.

But there are costs to owning a home that I think get overlooked, and there seems to be a stigma associated with renting: that if you are renting then you must just not be able to afford a house.

Costs of Renting vs Buying a House

Let’s not get into calculations just yet. First, I want to highlight the different types of costs (financial or not) that come with owning a house, and how they compare to renting.

Financial Costs

- Buying: the big deposit, stamp duty and other purchase costs, selling costs, the ongoing repayments, body corporate, council fees, and responsibility for everything about the house

- Renting: a tiny rental bond, smaller monthly rental payments, and responsibility only for the items you fill the house with and any damage done to the property (e.g. the burst water system was a hassle for us but didn’t cost us a thing to fix)

Opportunity Costs

- This is a big one. Locking yourself into home ownership restricts you in a number of ways:

- That deposit you put into your house could have been used for other things. For example:

- Other investments, like a share portfolio

- Your own business

- A safety net for unexpected financial circumstances

- That loan that you have to pay back each month needs to be paid or else your home could be forcibly sold by the bank

- This can make you really conservative in your financial actions and could lead to you clinging to job security even though you might be better off moving from your current job. For example, your boss is a dick and you’re currently being pushed around by him. If I were you, I’d try to sort things out so that you’re happy at work and if your boss threatens to fire you, just look for a job elsewhere. But fear is a very controlling emotion, and you might be settling for less because you’re afraid of your ability to keep the money flowing in for your loan repayments. Additionally, the thought of starting your own business, something you’re really passionate about, probably doesn’t stay in your mind for long as the fear of “what if the business doesn’t make money?” overpowers your desire to live a more fulfilling life

- That deposit you put into your house could have been used for other things. For example:

- In contrast, renting is full of flexibility

- That deposit money can be used for all three things listed above: a safety net so that the prospect of being out of work for a month isn’t an issue, and so that unexpected costs don’t stress you out; some money in other investments like shares; and the rest is available so that you can try starting your own business without the need for it to be bringing in money straight away — the money is time, allowing the business to grow to a point where it can start bringing in profits

- Moving is easy

- If you moved into your house and didn’t end up being happy with a particular aspect or the neighbours, just move at the end of the lease. No selling costs, just a few hundred dollars to get help moving your stuff from one house to the next and a weekend of hassle sorting out address changes, etc

- If a job opportunity comes up interstate or overseas, you can easily take it

- You can start in a small, basic home then upgrade every few years to a nicer and nicer home, or as your family composition changes

- However, renting is beaten by ownership in some areas:

- Owning means you have no landlord who can kick you out at the end of your lease

- Renters often have restrictions on ability to modify the house. For example, we aren’t allowed to put hooks in the walls to hang things from them, neither can we change the carpets or repaint the walls, etc

As you can see, there is a bigger cost to ownership than just the financial, which can often be much more important.

The Financial Difference

As an alternative to my usual number crunching, you can watch the video below by Khan Academy. It’s about 10 minutes long and walks you through the numbers. Alternatively, I will go through some real life examples below that you might find more relatable and quicker to digest.

Please note that the video is American. Australians do not get to deduct interest payments for a personal residence from their income to reduce their tax. However, you do not have to pay tax on any appreciation in value, if any.

My Example

From a quick search on realestate.com, one of the cheapest rentals I could find in Ringwood, Victoria was an old 2 bedroom unit1 for $320 p.w. A similar, old 2 bedroom unit in Ringwood recently sold for $420k2.

Assumptions for simplification:

- You never leave the house, so there’s no sale and there are no moving costs

- You get an interest-only loan on the house, not a principle-and-interest (P&I)

- P&I loans involve interest only loan repayments plus a bit extra to slowly chip away at the loan owed. The ‘extra’ is essentially being put into an investment with a guaranteed return equal to the interest rate on your loan. We could complicate things by using a P&I loan for the buyer and a share portfolio for the renter, but let’s keep things simple

- You take out no home or contents insurance, and you don’t encounter any repair jobs

- The property price doesn’t change, and the renter doesn’t invest the deposit money in shares, just cash. This removes investment risk from the comparison

The opportunity cost of the buyer is factored in by assuming the renter has the same amount of money in the bank, earning interest at the current rates of 3% p.a.

| BUY | RENT |

|---|---|

| 20% deposit: $84k | $84k in the bank @ 3%: +$210 pm |

| Purchasing costs3: $18.6k | $18.6k in the bank @ 3%: +$45 pm |

| 5% p.a. 5-year fixed interest-only loan repayments4: -$1,400 pm | Rent: -$1,390 pm |

| Total cost per month: $1,400 | Total cost per month: $1,135 |

| Note, that this is all “money burnt” — the cost to live in a home. Just as your rental payments don’t amount to anything in the future, neither do your loan repayments. In this example, you are $265 or almost 20% better off renting than you are buying. Not to mention that the purchasing costs are gone forever for the buyer, but the renter still has the money. If the renter withdrew the purchasing costs over 5 years, the renter would actually be receiving $350 a month, not $45. If it was 10 years, then $200, not $45. If 30, $100, not $45. | |

But Ash, Don’t Properties Always Go up in Value?

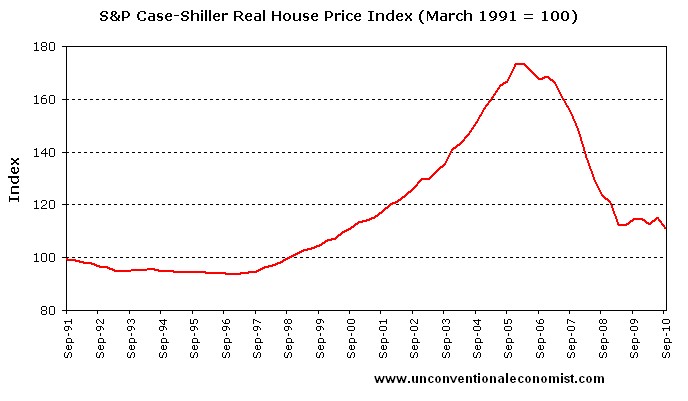

Short answer: No. See the GFC5

Long answer: almost all investments, if held long enough, increase in value over time. But asset prices often move in cycles — there might be a general trend upwards but there are smaller movements up and down over time. If you were to buy at the top of the cycle, then your investment is losing money over the next few months or years until the cycle picks up again. Just because you don’t sell during that time doesn’t mean you didn’t lose money (think about it: you could have rented for a year or two, then purchased closer to the bottom of the cycle).

What this question is getting at is the realisation that, in addition to paying money to live in a home, you have invested money into a house. This asset can go up or down in value — you have exposed yourself to investment risk. For this reason, buying a property instead of renting can actually be a bad investment decision. Sales agents, family, or friends might try to convince you otherwise (out of self-interest or ignorance) by appealing to a need for shelter or security or something, but in reality, you can rent for a year or two until (if) it actually makes sense to buy.

Property prices in Australia recently jumped up over the last year or two and there are plenty of articles6 quoting financial analysts who say the housing market is going to “correct” (decrease to prices more in line with expectations and affordability) this year, as is already starting to happen7. If you’re looking at moving out any time soon, be very careful about how much you borrow, where you are purchasing, and what type of property you are looking at, and seriously consider renting for a couple of years while the market is flat (do your research).

Exactly When to Buy or Rent

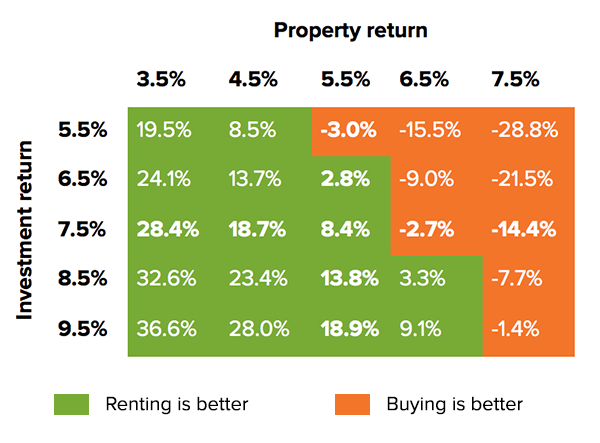

Assuming you don’t mind locking your money up in a property (instead of, say, using that money to start your own business) and that you mainly care about the financial side of living out of home, SBS put together a nice table:

Image source: sbs.com.au

In our simplified calculations above, we assumed no movements in investment values: the property price didn’t change and the renter didn’t invest the deposit money in shares, just cash. The image above does factor them in, which is good as it more accurately reflects reality. The article makes a number of assumptions, with are worth checking out (click the hyperlink under the image), but the main idea is that the difference depends on what the investment options are likely to do in the future. Since we don’t know, we can see what would be the better option with different scenarios.

On the vertical axis is the 7-year return you might expect to get in the share market (this is where the renter would put their ~$100k of savings). On the horizontal axis is the 7-year return you might expect to get in the property market (this is where the buyer is putting their $84k + purchasing costs). What you do is pick the two returns you think might occur in the next seven years for each asset class and then look at the number they intersect at in the table. This number is how much better (green and positive) a return the renter would get on their money over seven years compared to the buyer, or worse (orange and negative).

Written in November 2015, the SBS’s analysis concludes that:

Our analysis agrees with the RBA that renters are likely to be better off than property owners over the next 7 years based on long-term assumptions. This is consistent with the RBA’s assessment that Australian property is 19% overvalued compared to renting.

Why I Am Renting

Based on the above analysis, you can probably understand without reading the below why I would choose to rent instead of buy in the current market conditions.

Regardless, here are my reasons:

- If I buy a property, I will almost always be better off renting a separate home instead of just owning the home I live in.

- I like to live in a new, modern, and low maintenance home. Accordingly, my first home is a 6-year old apartment, designed according to my partner’s and my tastes. However, if I put money into property, I want to be able to manufacture capital growth, not just hold the property and hope that it appreciates. This involves buying a home that can be renovated or developed in the future, then sold at a profit. Since these properties are likely to not be new or modern, I’d rather not live in them.

- Although I gave up after 5 minutes of searching for evidence, I believe the rental yield8 on really expensive properties is much lower than the yield on more affordable properties, due to lower rental competition. Accordingly, you’re generally better off financially by renting amazing houses than actually owning them. So, depending on how much structural control we want over our future awesome house, we might still be renting.

- The opportunity cost of tying up my money was too big

- In our simplified comparison of the costs of renting vs buying, the renter just put their deposit money into the bank to earn 3% p.a. In the table by SBS above, the assumption is that the renter invests the money into a share portfolio, earning about 7.5% p.a. But it’s possible to earn an even higher return on your money if you can create a successful business, which is what I’m in the process of doing. After the return on your money goes to 10%, 20% or beyond, it doesn’t matter what the property prices do, it’s never going to be worth my while tying up my initial savings up in property.

- I don’t want the restriction

- Getting a loan requires that you have a stable and consistent income to fund it. In other words, it would mean I would have to: (a) have gone straight into a typical graduate position in Accounting; or (b) wait a year or two until my businesses bring in enough consistent income that the bank would give me a loan. Since I believe I’m much better off running my own business, I wasn’t going to get a loan any time soon.

- The property market seemed to have hit a peak

- Given the above four points, I didn’t bother spending a week or two researching the property market and developing a more accurate opinion of what property prices were going to do. Regardless, it seems my assumption was valid. Buying just any property this year seems to be a bad move. You’d have to dig around for the perfect house in the perfect area to get a decent return.

Conclusion

It wasn’t the right decision for me to buy a property, and based on the renting vs buying comparisons above, renting is probably the better option for you as well, if you’re in Australia. When you do want to make a decision, compare both options and choose the one that best fits your goals. Buying a property is a big decision that has medium to long-term consequences — you don’t want to lock into that kind of decision unless you’re sure it’s the best option for you.

Link here, although I don’t know how long the link will work for ↩

Calculator says Mortgage fee of $114, Title transfer of $1,173, and Stamp Duty of $17,370 ↩

$336k loan (80%) × 5% ↩

sort of like the interest rate on your money in the bank: it’s the rental you get every year divided by the price you paid for the property ↩